All Categories

Featured

Table of Contents

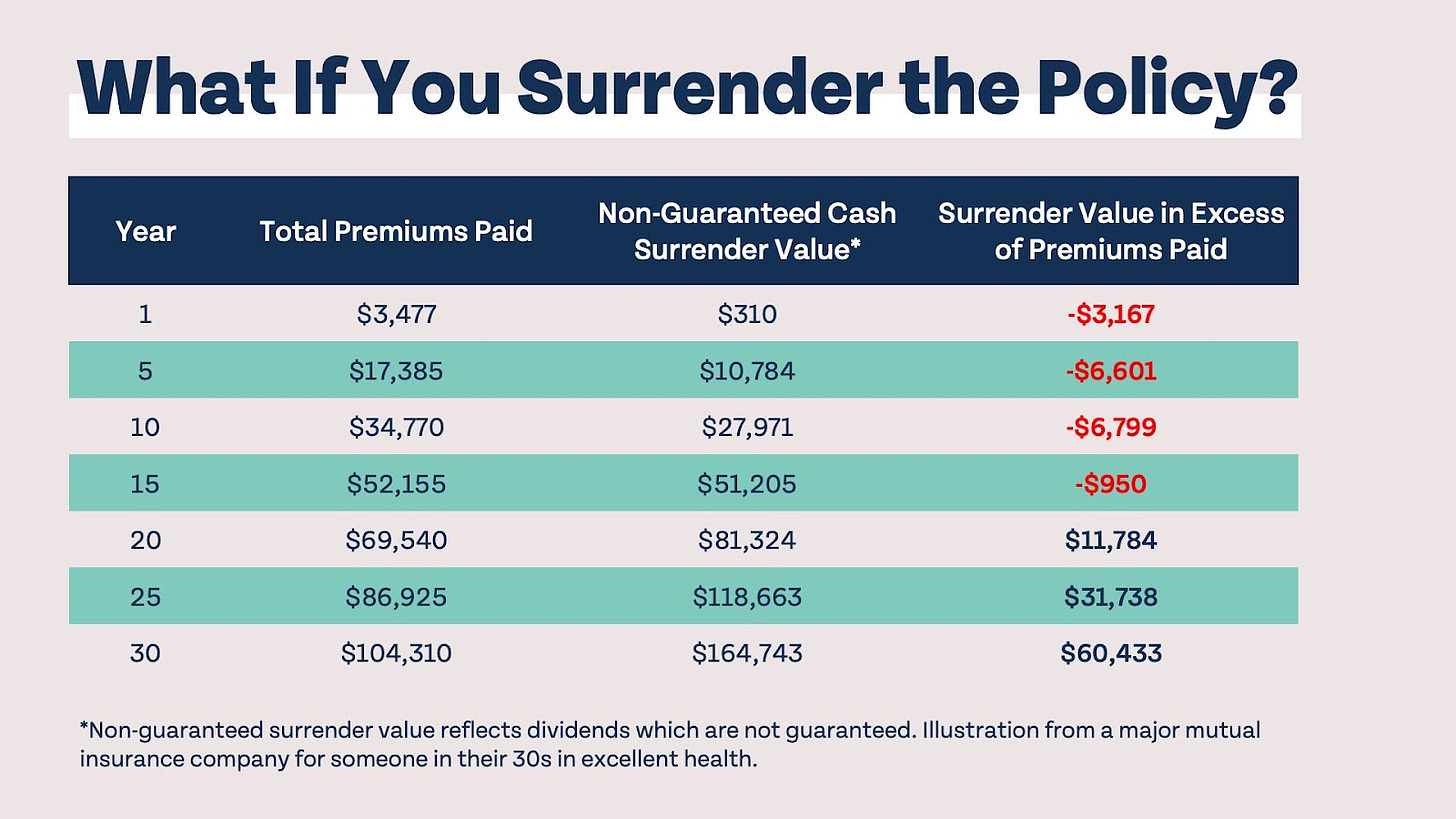

For the majority of people, the biggest issue with the limitless banking principle is that first hit to early liquidity triggered by the costs. Although this con of boundless financial can be reduced considerably with appropriate policy layout, the first years will certainly constantly be the most awful years with any type of Whole Life policy.

That stated, there are specific boundless banking life insurance policy policies designed mostly for high early cash money value (HECV) of over 90% in the initial year. However, the lasting performance will certainly frequently substantially lag the best-performing Infinite Financial life insurance policy plans. Having access to that added four numbers in the very first few years may come with the price of 6-figures later on.

You really obtain some significant long-term benefits that assist you recoup these very early expenses and after that some. We find that this impeded early liquidity issue with limitless banking is extra mental than anything else when extensively discovered. If they definitely required every penny of the money missing from their boundless banking life insurance plan in the initial couple of years.

Tag: unlimited banking concept In this episode, I chat regarding financial resources with Mary Jo Irmen that instructs the Infinite Banking Concept. With the rise of TikTok as an information-sharing system, monetary recommendations and strategies have actually located a novel method of spreading. One such technique that has been making the rounds is the infinite banking idea, or IBC for brief, garnering recommendations from celebrities like rap artist Waka Flocka Flame.

Within these plans, the money value expands based on a price set by the insurance provider. As soon as a significant cash money worth builds up, policyholders can get a cash worth lending. These financings differ from standard ones, with life insurance policy offering as security, indicating one might lose their coverage if loaning excessively without appropriate money worth to sustain the insurance coverage expenses.

And while the appeal of these policies is apparent, there are innate limitations and risks, requiring persistent money worth tracking. The technique's legitimacy isn't black and white. For high-net-worth people or company owner, specifically those using approaches like company-owned life insurance policy (COLI), the benefits of tax breaks and compound development might be appealing.

How To Be Your Own Bank

The allure of limitless banking doesn't negate its challenges: Cost: The foundational requirement, a permanent life insurance policy plan, is pricier than its term counterparts. Qualification: Not everyone gets whole life insurance policy as a result of extensive underwriting procedures that can omit those with details wellness or lifestyle problems. Complexity and risk: The complex nature of IBC, paired with its threats, may deter lots of, specifically when easier and less risky alternatives are available.

Allocating around 10% of your monthly revenue to the plan is just not practical for the majority of people. Utilizing life insurance policy as an investment and liquidity source requires technique and surveillance of policy money worth. Get in touch with a financial advisor to figure out if unlimited banking aligns with your priorities. Part of what you review below is simply a reiteration of what has already been claimed above.

So before you obtain right into a scenario you're not planned for, recognize the following initially: Although the concept is commonly marketed as such, you're not actually taking a lending from on your own. If that held true, you would not have to settle it. Rather, you're obtaining from the insurance business and need to repay it with passion.

Some social media messages recommend using cash value from entire life insurance coverage to pay for credit rating card debt. The idea is that when you pay back the funding with rate of interest, the quantity will be sent out back to your financial investments. Sadly, that's not exactly how it functions. When you repay the financing, a section of that rate of interest goes to the insurance coverage firm.

For the first a number of years, you'll be paying off the commission. This makes it extremely challenging for your plan to collect value throughout this time. Unless you can pay for to pay a few to numerous hundred dollars for the following years or more, IBC will not function for you.

Dave Ramsey Infinite Banking Concept

If you require life insurance coverage, below are some useful suggestions to take into consideration: Consider term life insurance. Make sure to shop around for the best price.

Copyright (c) 2023, Intercom, Inc. () with Booked Font Name "Montserrat". This Typeface Software application is accredited under the SIL Open Font License, Variation 1.1. Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Booked Typeface Name "Montserrat". This Font Software application is licensed under the SIL Open Font Style Certificate, Variation 1.1.Miss to major web content

Free Infinite Banking Videos

As a CPA focusing on realty investing, I've brushed shoulders with the "Infinite Financial Idea" (IBC) more times than I can count. I've also spoken with specialists on the subject. The primary draw, other than the obvious life insurance benefits, was constantly the idea of building up cash money worth within a permanent life insurance policy plan and borrowing versus it.

Certain, that makes good sense. Honestly, I always thought that cash would be much better spent straight on financial investments rather than channeling it via a life insurance plan Until I found just how IBC can be combined with an Irrevocable Life Insurance Trust (ILIT) to create generational wide range. Let's begin with the basics.

Specially Designed Life Insurance

When you obtain versus your policy's cash worth, there's no set payment schedule, providing you the freedom to handle the financing on your terms. The money worth continues to grow based on the policy's assurances and dividends. This arrangement allows you to access liquidity without disrupting the long-term growth of your policy, gave that the lending and interest are managed sensibly.

As grandchildren are birthed and expand up, the ILIT can acquire life insurance coverage plans on their lives. Family participants can take lendings from the ILIT, making use of the cash worth of the policies to money investments, begin organizations, or cover major expenses.

An important aspect of managing this Family Bank is making use of the HEMS requirement, which represents "Wellness, Education And Learning, Maintenance, or Assistance." This guideline is usually included in count on contracts to direct the trustee on exactly how they can distribute funds to beneficiaries. By adhering to the HEMS standard, the count on makes sure that distributions are created necessary demands and long-lasting support, safeguarding the depend on's properties while still offering relative.

Enhanced Versatility: Unlike inflexible small business loan, you manage the settlement terms when obtaining from your very own plan. This allows you to framework payments in a manner that lines up with your company capital. td bank visa infinite. Enhanced Capital: By financing service expenses via plan fundings, you can possibly liberate money that would or else be linked up in typical finance payments or devices leases

He has the same equipment, however has actually additionally developed extra money worth in his plan and obtained tax obligation benefits. And also, he currently has $50,000 available in his plan to make use of for future possibilities or expenditures. In spite of its potential benefits, some people stay hesitant of the Infinite Financial Idea. Let's address a few common worries: "Isn't this simply expensive life insurance policy?" While it holds true that the premiums for a correctly structured entire life policy may be greater than term insurance coverage, it is necessary to view it as even more than just life insurance.

Infinite Bank Concept

It's concerning creating a flexible funding system that provides you control and gives numerous advantages. When utilized tactically, it can enhance other financial investments and business methods. If you're captivated by the possibility of the Infinite Financial Idea for your business, here are some actions to take into consideration: Inform Yourself: Dive much deeper right into the concept through reputable books, workshops, or appointments with well-informed professionals.

{kind=link}

Latest Posts

Infinitebanking.org

Ibc Personal Banking

Non Direct Recognition Whole Life Insurance